Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Massachusetts is one of the most competitive housing markets in the country. Between rising home prices and high rental demand, many people are asking themselves the same question: Is it smarter to rent or buy right now?

Let’s break down the numbers and look at why buying often comes out ahead.

The Cost of Renting in Massachusetts

According to recent rental data, the average rent in Massachusetts for a 2-bedroom apartment is between $2,500–$3,200 per month, depending on location. In Greater Boston, it’s not uncommon for rents to push $3,500+ for a modest unit.

While renting offers flexibility, the biggest drawback is that 100% of your rent payment goes to your landlord. You don’t build equity, and your housing cost can increase every year when your lease renews.

The Cost of Buying in Massachusetts

Now, let’s compare renting with buying.

-

Example Home Price: $500,000

-

Down Payment: 5% ($25,000)

-

Loan Amount: $475,000

-

Interest Rate: ~6.5% (subject to change)

-

Property Taxes & Insurance: ~$600/month

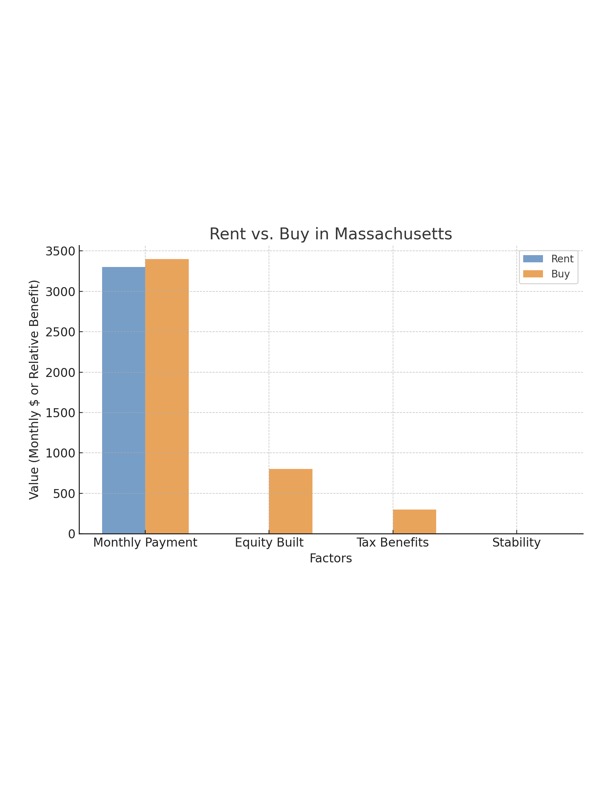

Estimated Monthly Mortgage Payment: ~$3,300–$3,400

That’s almost identical to what many renters are already paying.

Key Difference: Equity

The critical difference between paying $3,300 in rent versus $3,300 on a mortgage is what happens to the money:

-

Rent: Gone forever, with no return.

-

Mortgage: A large portion goes toward interest early on, but every payment chips away at your loan balance. Over time, you’re building equity in an asset that’s appreciating.

If your home appreciates just 3% per year (a conservative number in Massachusetts), that $500,000 home could be worth over $580,000 in 5 years — while you’ve also paid down the loan.

Other Advantages of Buying

-

Fixed Housing Costs: With a fixed-rate mortgage, your monthly payment stays steady. Rent, on the other hand, typically increases every year.

-

Tax Benefits: Homeowners may deduct mortgage interest and property taxes (consult a tax professional for specifics).

-

Stability: You control your living situation — no landlord deciding whether to sell or raise rent.

Final Thoughts

When rent and mortgage payments are nearly the same, buying often comes out ahead — especially in Massachusetts, where home values have historically appreciated faster than the national average.

While buying does require upfront costs (down payment, closing costs, and maintenance), the long-term financial upside is hard to ignore. Renters keep paying into someone else’s investment, while buyers build wealth for themselves.

Programs That Make Buying Easier

If saving for a down payment is the biggest hurdle, there are programs available in Massachusetts that can help:

-

Conventional 97 Loan – Allows buyers to put as little as 3% down.

-

FHA Loan – Requires only 3.5% down, with flexible credit requirements.

-

MassHousing Down Payment Assistance – Offers up to $25,000 in down payment help for eligible buyers in Massachusetts.

-

First-Time Homebuyer Programs – Many local cities and towns also offer grants or forgivable loans to assist with down payment and closing costs.

These programs make it possible to buy a home with much less upfront savings than most renters realize.