Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The average down payment for a house in Massachusetts can vary depending on a variety of factors, including the price of the home and the type of loan being used to purchase it. However, generally speaking, the average down payment in Massachusetts is around 20% of the purchase price of the home.

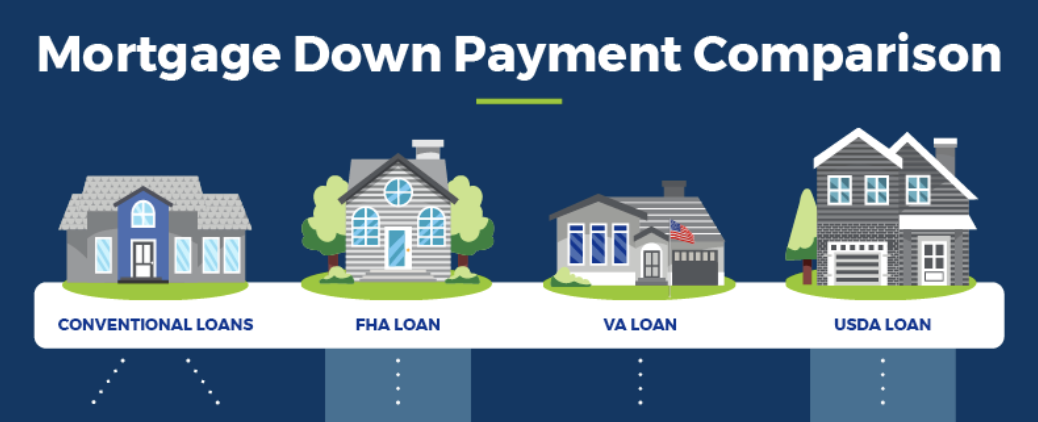

While 20% is the typical down payment required by lenders to avoid paying private mortgage insurance (PMI), it’s possible to purchase a house with a smaller down payment. For example, government-backed loans such as FHA loans only require a 3.5% down payment. Conventional loans also have options such as 5% or 10% down payment.

It’s important to note that the size of the down payment also affects the mortgage interest rate. The larger the down payment, the lower the interest rate will be. This is because a larger down payment reduces the risk for the lender and makes the loan more secure.

Additionally, in Massachusetts, there are programs that offer down payment assistance for first-time homebuyers, veterans, and low-income buyers, such as Massachusetts Housing Partnership (MHP) One Mortgage and the Massachusetts Affordable Housing Alliance (MAHA) program. These programs can help buyers with down payments as low as 3% and can also provide assistance with closing costs.

In summary, the average down payment for a house in Massachusetts is around 20% of the purchase price, but it’s possible to purchase a house with a smaller down payment. Government-backed loans such as FHA loans require a 3.5% down payment and conventional loans have options such as 5% or 10% down payment. However, the size of the down payment also affects the mortgage interest rate, and in Massachusetts, there are also programs that offer down payment assistance for first-time homebuyers, veterans, and low-income buyers that can help buyers with down payments as low as 3%.